|

In 2011, Marfrig made significant progress in regard to the execution of its long-term strategy, consolidating its position as a global food company focused on the generation of results and the sustainability of its business. Due to divisional integration, the capture of synergies and a focus on our core business and operating efficiency, we managed to obtain gains in our production structure and build a high value-added product portfolio with brands that have strong proximity with our consumers.

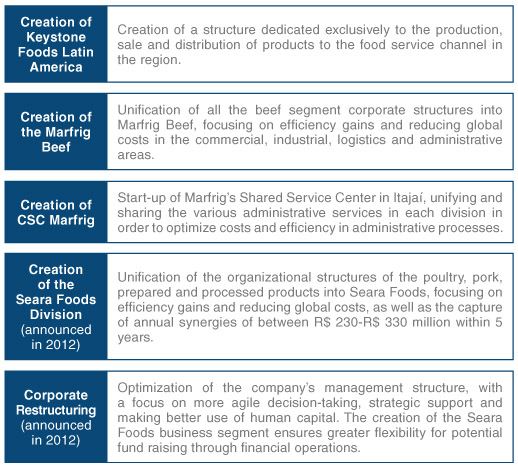

We streamlined our organizational structure, favoring the capture of synergies in all divisions and resulting in an increased emphasis on business management, cost reductions and the generation of cash flow. This process was developed in conjunction with the consulting firm, Bain & Company and took place in two stages, announced in October 2011 and February 2012.

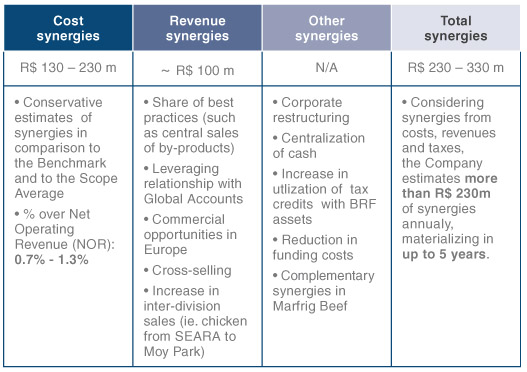

Our poultry, pork, prepared and processed food operations were consolidated into Seara Foods, which was created to optimize our production, commercial and logistics base and facilitate the capture of synergies. As part of the same strategy, we created Marfrig Beef to consolidate our beef, lamb and leather operations into a single business unit to boost operational efficiency. This new consolidation should generate cost and revenue synergies of between R$ 230 million and R$ 330 million within five years.

We continue to maintain strict control over investments in fixed assets and working capital accounts and to operate with financial discipline, aiming to increase operating cash flow in 2012.

We increased the share of value-added and processed products in our sales, which climbed from 28.0%, in 2010, to 37.4%, fueled by the acquisition of Keystone Foods, investments in the brand Seara and Seara’s new products launch like lasagnas, ready-to-eat meals, pizzas, sliced products and sandwiches, as well as special beef cuts. In addition to expanding its national presence, Seara launched several product lines targeting the export market, including hamburgers, breaded products and ready-to-eat meals, which were shipped to South America, Europe, Asia and the Middle East.

Our strategy of further strengthening the Seara brand was reinforced by a binding agreement for the exchange of assets entered into with BRF S.A. in December 2011. Once concluded, this will allow us to gradually increase our domestic sales and practically double our Brazilian nominal installed production capacity of processed and value-added products by 2013. As a result, we will be closer to our goal of generating 50% of our revenue from this product category and increasing the stability of our operating margins.

In order to take advantage of the growing opportunities in the Chinese market and expand our presence in that country, which we consider one of the major drivers of global protein demand growth, we established two Chinese joint ventures through Keystone Foods, one of which, Keystone-Chinwhiz (60% Keystone - 40% Chinwhiz), is building a vertically integrated poultry production chain, which began 2012 processing around 200,000 birds per day. In addition, Marfrig was the first Brazilian company authorized to export pork products to China, once again underlining its capacity to adjust rapidly to client and market needs.

Aware of our responsibilities in the sustainability area, in 2011 we initiated the consistent global mapping of our greenhouse gas (GHG) emissions throughout the entire production chain. The result was our first global emission report, which will serve as a platform for the implementation of a series of environmental programs designed to lead us towards a low-carbon economy. We also prepared our first Annual Sustainability Report based on Global Reporting Initiative (GRI) guidelines.

Finally, we are very proud to have received market recognition for our achievements, having been one of the winners of the 2011 Transparency Trophy, granted by Anefac, Fipecafi and Serasa Experian, the first time a food company has been so honored. We were also elected “Best Meat Company” by Exame magazine’s Biggest and Best guide and “Best Meat Company” by Globo Rural magazine.

We are confident that we are on the right path towards achieving our long-term objectives of building a food company that is a benchmark for sustainability, with increasing and sustainable margins, and creating value for the production chains and our shareholders. Our initiatives and priorities in 2012 include:

• Operational improvements and the capture of synergies from the corporate restructuring;

• Cost and expense reductions and efficient working capital management;

• Strict control over working capital needs, always seeking a balance between cash flow and capital structure;

• Conservative cash and debt profile, with a focus on deleveraging;

• Increasing the share of prepared and processed products and pursuing sustainable margins in the long term;

• Focus on the Food Service market through Keystone Foods;

• Growth in the Asian (mainly Chinese) and Brazilian markets.

To achieve these goals, I would like once again to count on the commitment of all of our 85,000 employees in our pursuit of sustainable results and growth, better opportunities and constant operational improvements.

In closing, I would like to once again thank all of Marfrig’s stakeholders who have been fundamental to our success: our employees, for their dedication and commitment; our clients and consumers, for their trust in the quality of our products; our shareholders, for their support and their confidence in the Group’s medium and long-term sustainable growth strategy; our suppliers, for their trust and ever stronger partnership; and our friends and everyone else who believes in Marfrig. We are only just at the beginning of a great future!

Marcos Antonio Molina dos Santos

CEO & Chairman

2. Corporate Profile

Marfrig Alimentos S.A. is a multinational company with operations in the food and service sectors in Brazil and abroad. Its activities are focused on the production, processing preparation, sale and distribution of animal protein (beef, pork, lamb and prepared products), pasta and similar (pizzas, lasagnas, breaded products, desserts etc.), ready-to-eat meals and frozen vegetables, as well as the distribution of other food products (frozen items, cold cuts, sausages and fish, among others) and semi-finished and finished leather.

On December 31, 2011, the Marfrig Group, which is headquartered in the city of São Paulo, operated throughout Brazil and in 21 other countries in 5 continents (Argentina, Uruguay, Chile, the USA, France, Northern Ireland, England, Holland, South Africa, Mexico, Germany, United Arab Emirates, Kuwait, Qatar, Bahrain, China, Thailand, Malaysia, South Korea, Australia and New Zealand), through 150 production units, distribution centers and commercial offices and a monthly production capacity of over 140,000 tonnes of processed products. It has a direct workforce of approximately 85,000 and exports to more than 160 countries in Europe, the Middle East, Asia and the Americas.

In 2007, the Group went public and was listed in the BM&FBovespa’s Novo Mercado trading segment, which contains only those companies with the best corporate governance practices.

As of 2012, the Group’s organizational structure (Chart 1) was divided into two major segments in order to improve operational efficiency, ensure more rapid decision-taking and pursue synergies among the various divisions:

Marfrig Beef, which comprises the beef divisions in Brazil, Argentina and Uruguay; and Chile.

Seara Foods (poultry, pork, prepared and processed products), comprising the operations of Seara (Brazil), Moy Park (Europe) and Keystone Foods (global).

This structure serves some 79,000 regional and global clients, including the food service market and major retail chains.

Chart 1 - Organizational Structure of the Marfrig Group.

Marfrig has a portfolio of solid, well-positioned and well-known brands that are symbols of high-quality food products, including Seara, Bassi, Montana, Tacuarembó and MoyPark. In addition, in 2011 the Group entered into a partnership with the chef Jamie Oliver to sell products under his brand in the UK. Seara remains strategically positioned as the Company’s global brand, with top-quality products at competitive prices in the domestic and international markets.

Managed by an experienced team committed to the highest standards of corporate governance and environmental responsibility, the Group has become consolidated as one of the global food industry leaders, being the fourth-ranked global animal protein producer and Brazil’s second-largest producer and exporter of poultry and processed products.

3. Corporate Strategy

The Marfrig Group’s strategy is based on the sustainability of its businesses over the long term and generating returns for its shareholders. To achieve these goals, the Company has adopted the following strategic pillars for the coming years:

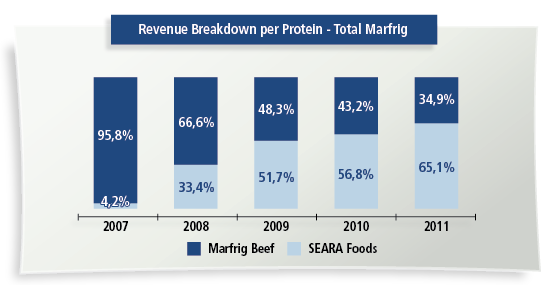

In line with the global consumption trend, where beef’s continuing position as the top-quality meat with stable demand, is being challenged by the growing share of poultry and pork, which are cheaper than other meats, Marfrig has been gradually expanding its share of the poultry, pork, value-added and processed product segment, represented by Seara Foods, which accounted for 65.1% of the Group’s total revenue in 2011. Graph 1 below shows Marfrig’s strategy of geographic and protein diversification, with the increased share of value-added products, adopted since the IPO in order to mitigate the risks inherent to the global market and the segments where it operates:

Graph 1 - Breakdown of the Marfrig Group’s revenue by segment.

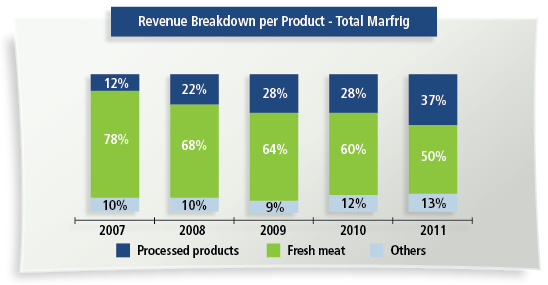

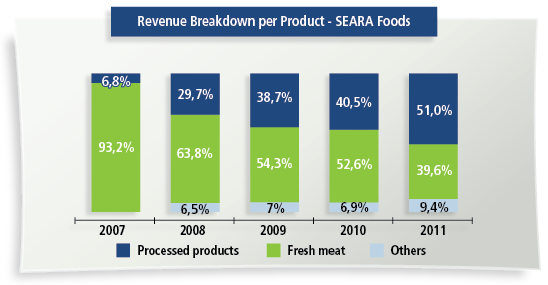

Also with the aim of increasing the share of higher value-added prepared and processed products, in its sales mix, Marfrig has been expanding the contribution of these items to its overall portfolio and the poultry, pork, prepared and processed product portfolio (Seara Foods), as shown in Graphs 2 and 3 below. In the long term, Marfrig aims to generate 50% of its revenue from higher value-added prepared and processed products. In 2011, these items accounted for 37.4% of the company’s portfolio.

Graph 2 - Breakdown of Marfrig Group revenue per product type.

Graph 3 - Breakdown of Seara Foods revenue per product type.

4. 2011 Highlights

Financial Highlights

• Net revenue of R$ 21.9 billion, 37.8% higher than the R$ 15.9 billion recorded in 2010. The organic growth of net revenue (compared with the pro-forma 2010 net revenue, which included the companies acquired in that year) stood at 12.1%;

• EBITDA of R$ 1.8 billion, 18.1% up on the R$ 1.5 billion posted in 2010;

• EBITDA margin of 8.1%, 140 bps down on the 9.5% registered in 2010, basically due to:

– The appreciation of the Real in the year through September, with a negative impact on exports;

– High grain and cattle prices;

– Inflationary pressure in some of the countries where we operate.

• Net loss of R$ 746.0 million, the bulk of which due to the non-cash impact related to the exchange variation of R$ 780.7 million in the period, versus net income of R$ 146.1 million in 2010.

Operating and Strategic Highlights

• Increase in the share of prepared and processed products, which have higher added value, to 37.4% of the Company’s net operating revenue, versus 28.0% in 2010;

• Consolidation and expansion of the Seara brand, with the launch of 77 products, the capture of synergies worth R$ 201.1 million (0.5% of the estimated amount), its increased market share in Brazil and its expanded presence in several markets in South America, Europe, Asia and the Middle East;

• Focus on the company’s core business, i.e. the production of protein-based products, especially prepared and processed items, which have higher added value, including the following measures:

• Focus on the consolidation of all divisions and the implementation of operational measures to optimize the organizational structure, management and the production platform, aiming to improve margins and profitability, led by the following initiatives:

5. Industry Performance

2011 was marked by substantial volatility and uncertainty in the international capital market, due to the European sovereign debt crisis and the stagnation of the U.S. economy. However, the U.S. has prospects of a recovery in 2012, despite still high unemployment (9.4% in December 2011).

On the other hand, the momentum of the emerging countries, fueled by their enormous and buoyant consumer markets, prevented a global recession, thus consolidating the asymmetry between the developed and developing nations.

In general, the emerging countries were less affected by the international crisis. In Brazil, GDP recorded modest growth of 2.7% over 2010, the Real depreciated by 12.6% to US$/R$ 1.8758 (on December 29, 2011) and inflation, measured by the IPCA consumer price index, recorded 6.5%, at the upper limit of the target established by National Monetary Council (CMN) and the highest annual figure since 2004. Nevertheless, unemployment fell to 9.1% in December 2011, the lowest ratio since 1990, and the expansion of earnings and credit continued to fuel household consumption and, consequently, the domestic market.

According to the IBGE, food and beverages, despite experiencing lower inflation in 2011 (7.18%, versus 10.39% in 2010), had the biggest impact on the IPCA, accounting for 23.46% of the total, due to higher raw material costs (finished cattle and grains) and strong pressure from the price of food eaten outside the home, which increased by 10.49% in 2011.

Chinese GDP grew by 9.2% in 2011, although the pace of growth at year-end was the slowest for ten quarters, reflecting slower global demand and the measures implemented by the Chinese government to curb inflation, which should further impact demand in 2012. Russia maintained a moderate GDP growth trajectory (4%).

The upturn in individual earnings, coupled with economic growth, growing urbanization and changes in the eating habits of the developing countries, especially China, have resulted in increased demand for agricultural commodities. This fact, together with relatively low global inventories, poor harvests in important producing regions due to adverse weather conditions, and the increasing allocation of maize and vegetable oils to ethanol and biodiesel production, all helped keep international commodity prices at elevated levels.

Average corn prices in Brazil (ESALQ) increased by 42.4% over 2010, while average soybean prices (ESALQ) moved up by 15.8%. Chicago Board of Trade (CBOT) prices were equally unfavorable, with corn, soybean and wheat (also used in the production of animal feed abroad) recording average upturns of 59.1%, 25.8% and 22.3%, respectively.

The South American beef market in 2011 was also marked by the high cost of finished cattle, which increased by an average 15% in Brazil (in Reais) and close to 32% in Argentina and Uruguay (in Argentine pesos and U.S. dollars, respectively), according to Argentina’s Agricultural Control Office (ONCCA) and Uruguay’s National Meat Institute (INAC), due to the slow recovery of the cattle production cycle and lean inventories in relation to demand. The Brazilian domestic market, driven by higher income and household consumption, remained exceptionally heated, allowing a greater proportion of output to be routed to the domestic market to the detriment of exports. According to the Brazilian Ministry of Development, Industry and Foreign Trade, exports totaled 1,097 million tonnes in 2011, 4.9% down on the year before, while internal annual per capita consumption came to 39.9 kg, versus 39.8 kg in 2010, according to the Food and Agricultural Policy Research Institute (FAPRI).

According to the Brazilian Poultry Association (Ubabef), Brazilian per capita poultry consumption increased by 7.5% over 2010 to 47.4 kg/year. Of the 13.1 million tonnes of chicken produced in Brazil (the third largest global producer) in 2011, 69.8% was allocated to the domestic market. According to the USDA, Brazilian per capita poultry consumption is the seventh highest in the world, behind the United Arab Emirates, Kuwait, Bahrain, Saudi Arabia, Jamaica and Qatar.

6. Operating and Financial Performance (2011)

Net Operating Revenue

The Marfrig Group recorded consolidated net revenue of R$ 21.9 billion in 2011, 37.8% more than the R$ 15.9 billion recorded in 2010, while organic net revenue growth (compared with pro-forma 2010 net revenue, which included the companies acquired that year) came to 12.1%. The main growth drivers were:

• Higher beef prices in Brazil and the excellent performance of the Food Service segment;

• Growth of the Poultry, Pork, Prepared and Processed Products (Seara Foods) segment, with the expansion of Seara in Brazil;

• The increased share of prepared and processed products, which have higher added value, in the Company’s sales mix.

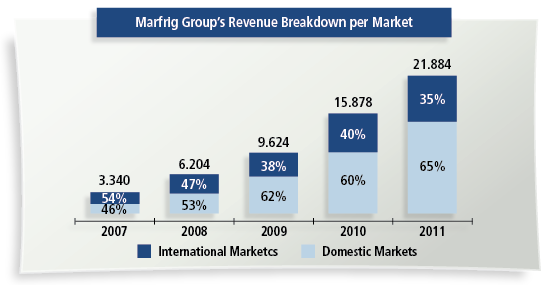

Graph 4 - Marfrig Group’s net revenue per market.

Graph 5 - Marfrig Group’s net revenue per product.

Domestic sales accounted for 65.0% of consolidated revenue, versus 60.0% in 2010, an indication that domestic market conditions remained favorable. Exports recorded a decline, reflecting the advantageous national scenario and the 35.3% appreciation of the Real through September 2011, versus 40.2% in the same period in 2010.

In regard to product diversification, the Seara Foods segment accounted for 65.1% of 2011 net revenue, versus 56.8% in the previous year, reflecting the Company’s strategy of increasing the share of these items in its mix.

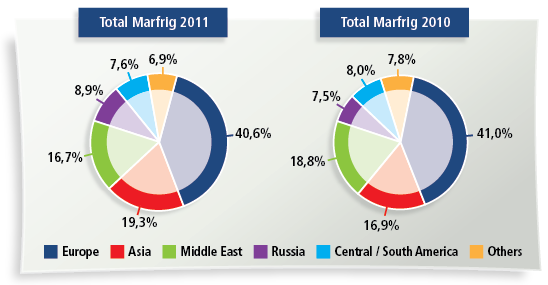

There follows a breakdown of net revenue by major export destination in 2011 and 2010. Europe continued to head the export rankings, followed by Asia and the Middle East. We remain directing our exports to more profitable regions.

Graph 6 - Breakdown of Marfrig Group revenue by export market in 2011 and 2010.

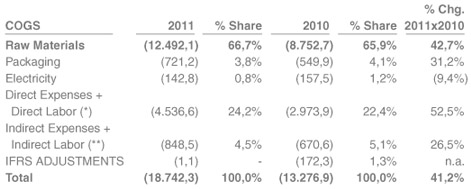

Cost of Goods Sold (COGS)

The cost of goods sold (COGS) climbed by 41.2%, from R$ 13,277.0 million, in 2010, to R$ 18,742.3 million, in line with the increase in revenue and raw material prices (cattle and grains), and organic growth in the Poultry, Pork, Processed and Prepared Product division.

(*) Direct expenses and direct labor

(**) Indirect expenses and indirect labor

Raw materials, which include animals and feed inputs (grains), remained the chief component of COGS, accounting for 66.7% of the total, in line with 2010.

The beef division represented 32.0% of COGS, while poultry, pork, prepared and processed food operations accounted for 68.0%. Within the beef division, cattle accounted for around 82% of COGS, while grains and meals accounted for close to 65% of the total in the poultry, pork, prepared and processed food operations

Gross Income and Gross Margin

Gross income moved up by 20.8% from R$ 2,601.4 million, in 2010, to R$ 3,142.6 million, while the gross margin stood at 14.4%, down 200 bps from 16.4% in the previous year, chiefly due to the higher raw material prices and inflationary pressure in certain countries where the company operates.

The upturn in gross income reflects the organic growth of revenue from sales. The Company remains focused on optimizing its product mix by increasing the share of prepared and processed products, which have higher added value and should reduce margin volatility. In addition, a number of initiatives were implemented in the last two quarters to improve operations, including the optimization of Marfrig’s industrial facilities, with the dilution of fixed factory costs and the streamlining of raw material purchases. Together with the corporate restructuring, these initiatives should result in sustainable margins in the medium-to-long term.

Operating Expenses (SG&A)

Selling, general and administrative (SG&A) expenses totaled R$ 2,284.2 million in 2011, 15.9% up on the R$ 1,970.2 million recorded in 2010, due to organic growth and investments in marketing and advertising associated with the development of the group’s brands, especially the global Seara brand.

SG&A expenses represented 10.4% of annual net revenue, 200 bps down on the 12.4% recorded in 2010. In addition to adopting a policy of strict control over expenses, the Company has captured important synergies by integrating the structures of the units acquired in recent years, enabling the exchange of best practices and the dilution of fixed costs and expenses.

EBITDA and EBITDA Margin

Marfrig’s consolidated EBITDA (earnings before interest, taxes, depreciation and amortization) came to R$ 1,773.8 million in 2011, an 18.1% improvement over the R$ 1,502.5 million posted in 2010. Excluding non-recurring events and the reversal of provisions for the contingency payment of OSI in 2011, adjusted EBITDA increased by 27.2%.

The EBITDA margin stood at 8.1%, versus 9.5% in 2010, due to the appreciation of the Real in 2011 through September, which jeopardized exports, higher grain and cattle prices, and inflationary pressure in certain countries where we operate. The adjusted EBITDA margin narrowed by 60 bps, due to the same factors cited above.

EBITDA growth was driven by:

• Organic growth;

• Operational improvements in Seara Foods and the Marfrig Beef division, reflecting the previously-mentioned initiatives implemented along the year;

• The pursuit of more profitable international markets and channels, which partially offset the reduction in exports over the previous year.

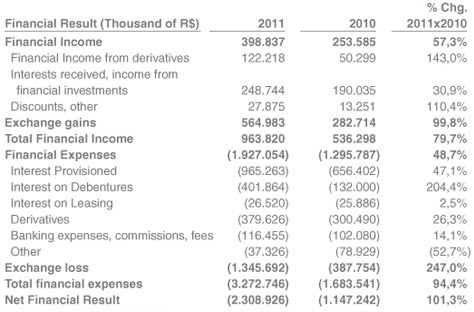

Financial Result

The 2011 financial result was a net expense of R$ 2,308.9 million, versus a net expense of R$ 1,147.2 million in 2010.

Given the 12.6% appreciation of the Real against the U.S. dollar in 2011, the Company recorded a net exchange loss (non-cash) of R$ 780.7 million, versus a loss of R$ 105.0 million in 2010.

Interest expenses increased by 71.1% in the year, reflecting the upturn in net debt due to investments in working capital, mainly in the first half, in turn due to higher raw material costs and the year’s funding.

Marfrig does not contract leveraged operations involving derivatives or similar instruments. The operations are designed to provide minimum protection against its exposure to other currencies, and maintains a conservative policy of not contracting operations that could jeopardize its financial position. The Company’s net loss from trading is explained by the hedging instruments detailed in note 31 to the standardized financial statements.

Net Income/Loss and Net Margin

The Company recorded a net loss of R$ 746.0 million in 2011, versus net income of R$ 146.1 million in 2010. The non-cash accounting impact of the R$ 780.7 million exchange loss on the dollar-denominated debt led the company to record a net loss in 2011.

However, it is important to note that Marfrig’s strategy of geographic and product diversification, combined with its globalized production platform and focus on prepared and processed products, should result in sustainable profitability in the medium-to-long term.

7. Performance by Business Segment

SEARA FOODS - POULTRY, PORK AND PREPARED AND PROCESSED PRODUCTS

2011 was marked by the integration of Keystone Foods and O´Kane Poultry, acquired in the end of 2010, into Marfrig’s international operations, consolidating the strategy of becoming a global food company, with a focus on increasing the share of higher added-value prepared and processed products in the sales mix. Other highlights included operational excellence, first-class customer service and successfully meeting the specific needs of each market.

Throughout the year, the Company concentrated on optimizing production and management processes, increasing the share of prepared and processed products, while investing in marketing, the Seara brand and the logistics operation, in order to increase the supply of products in the domestic market and bring the Seara brand closer to consumers.

In February 2012, Marfrig hired David Palfenier as the CEO of Seara Brasil. With his experience in processed and value-added products, David will lead Seara to a new phase of its development strategy, with sustainable growth in the national and international markets.

In February 2012, the Company announced a corporate restructuring of the Poultry, Pork, Prepared and Processed Product segment, with the integration of all three divisions (Seara Brasil, MoyPark and Keystone) under Seara Foods, in order to optimize production, sales and logistics.

This consolidation should generate cost and revenue synergies (in addition to the previously announced synergies of Seara Brasil) of between R$ 230-R$ 330 million per year within 5 years, as shown in the table below.

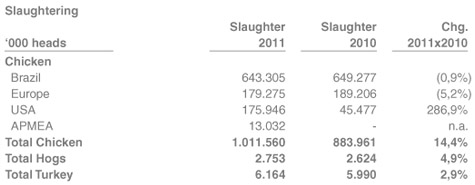

In 2011, Seara Brasil processed 643.3 million head of chicken, 0.9% down on the 649.3 million recorded in 2010, and 2.753 thousand hogs, up 4.9% from 2.624 thousand in 2010.

In the same period, poultry and hog slaughter volume in Brazil grew by 9.4% and 6.9%, respectively. In 2011, Marfrig’s share of total Brazilian poultry slaughter volume was 12.5%, versus 13.8% in 2010, while its share of hog slaughter edged up from 8.8%, in 2010, to 8.9%.

International operations processed 367 million head of chicken in 2011, 56,8% more than the 234 million processed in 2010, explained by the annualized effect of the Keystone Foods operations and organic growth. Also in 2011, Marfrig began poultry production in China through a joint venture with Chinwhiz, having recorded slaughter volume of 13.0 million chickens in the year.

Operations in Brazil and Europe jointly produced 6.2 million head of turkey, 2.9% up on the 6.0 million registered in 2010.

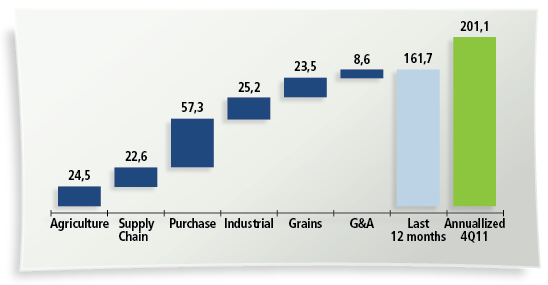

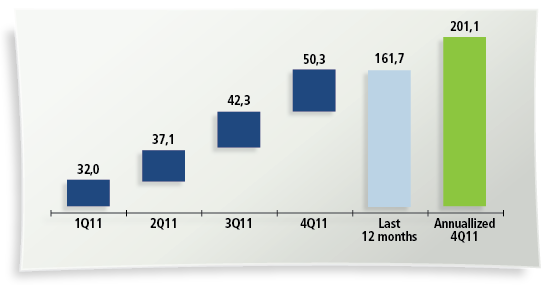

Despite the challenging scenario in 2011, including high grain prices and the appreciation of the Real, the synergy gains from the Seara operations came to R$ 201.1 million, 0.5% above the original estimate.

Graph 7 - Breakdown of synergies from the Seara operations.

Seara Brasil’s market share of the frozen meat segment increased by 1.9 p.p. thanks to distribution and marketing efforts throughout the year, which included national campaigns and the sponsorship of sports teams, in addition to the launch of 77 prepared and processed products.

With the aim of increasing the production capacity of prepared and processed products and strengthening the Seara brand in Brazil, on December 8, 2011, Marfrig signed a binding agreement with Brasil Foods S.A. (“BRF”) for the exchange of those assets detailed in the Performance Commitment Agreement (TCD) - which include 8 prepared and processed product plants, 8 distribution centers, and the Rezende, Confiança, Wilson, Fresky, Texas Burger, Doriana, Patitas, Fiesta, Escolha Saudável, Delicata, Tekitos and Excelsior brands - for hog units in Mato Grosso, certain assets in Argentina, including cattle processing and slaughter units, and the Paty brand.

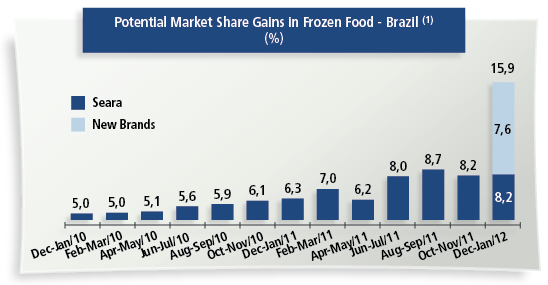

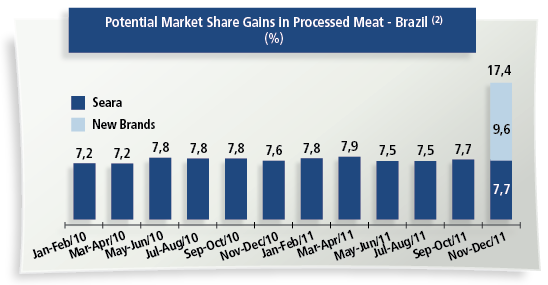

Graph 8 - Seara’s potential market share of the Brazilian market in the frozen meat

and prepared and processed meat segments. (Source: AC Nielsen)

(1) Frozen meats: meatballs, cuts, hamburgers, kebbeh, ready-to-eat snacks, nuggets, ready-to-eat dishes, stuffed products, savories, steaks and pies.

(2) Prepared and processed meat products: pressed meats, pressed ham, healthy meats, coppa, sausages, bologna, Parma ham, ham, salami and wieners.

When operating at full capacity, the brands originating from the transaction have the potential to increase Marfrig’s market share of processed and frozen products by 9.6 p.p. and 7.6 p.p., respectively, according to Nielsen’s latest figures. However, the integration of these assets will be a gradual process, as will the trajectory towards full capacity.

On the production side, when operating at full capacity, the new assets should increase Marfrig’s slaughter of chicken and hogs by more than 20% and more than double its installed processed and prepared product capacity, as shown below.

Graph 9 - Potential increase in installed capacity after the exchange of assets.

Seara Brasil’s exports delivered a solid performance, especially as of the third quarter with the devaluation of the Real against the U.S. dollar. According to SECEX, Marfrig recorded a 22.2% share of Brazil’s poultry exports in 2011, versus 20.5% in 2010, and a 15.0% share of pork exports, against 12.9% in the previous year.

Graph 10 - Seara’s share of Brazil’s total poultry and pork exports.

Europe, Asia and the Middle East absorbed most of Seara’s exports, as shown below. Shipments to Asia moved up over the year before and we expect a further substantial increase in the future thanks to the beginning of pork exports to China in November 2011 and the possible opening of this market to poultry exports.

Graph 11 - Breakdown of Seara’s exports by market in 2011 and 2010.

Also in an effort to optimize its operations, in 2011 Marfrig structured Keystone Foods Latin America, which specializes in the production, sale and distribution of products for the food service channel. The unification should generate operating gains from an innovative and diversified portfolio in a segment that regularly records annual double-digit growth, according to the Brazilian Food Industry Association (ABIA).

On the international front, in 2011 Keystone Foods established two joint ventures with Chinese companies:

• COFCO Keystone Foods Supply Chain (China) Investment Company (45% Keystone - 55% COFCO), for the construction of six distribution centers in strategic cities in China as of 2012; and

• Keystone-Chinwhiz Poultry Vertical Integration (60% Keystone - 40% Chinwhiz), for the creation of a vertically-integrated poultry chain, with a daily slaughtering capacity of 200,000 birds, which was already achieved in early 2012.

In line with its strategy of focusing on its core business, in 2011 the Company accepted a proposal to sell the specialized logistics services of Keystone Foods in the USA, Europe, the Middle East, Asia and Oceania to The Martin-Brower Company, for US$400 million, to be received on the conclusion of the transaction. Marfrig believes that the resulting focus on its protein business will add more value to clients in the fast food market.

The European operation performed well in 2011, mainly driven by chicken consumption in the United Kingdom. Moy Park continues to lead the UK chicken market, with a strong presence in major retail chains and in the food service segment. In March 2011, it was appointed as the biggest company in Northern Ireland by the “The 100 Largest Companies in Northern Ireland” year-book, published by the Belfast Telegraph. Throughout the year, it developed several marketing campaigns to strengthen the Moy Park brand in the UK and Europe, and entered into an agreement with the renowned British chef Jamie Oliver for the production and sale of a premium line of organic chicken products under his own brand name.

The overall strategy for the Poultry, Pork and Prepared and Processed Product segment is based on the following assumptions:

• Increasing the share of prepared and processed products, which have higher added value, in the Company’s sales mix;

• Expanding the Seara brand in Brazil and abroad;

• Capturing synergies from the integration of Seara Foods’ various global operations;

• Using products from South America, offering an increasingly broad and comprehensive portfolio of high-quality, competitive products;

• Focusing on the Brazilian and Chinese markets, where protein consumption is expected to increase substantially in the coming years.

MARFRIG BEEF - BEEF, LAMB AND LEATHER

In 2011, we unified the corporate structure of beef operations in Brazil, Argentina and Uruguay under the Marfrig Beef division in order to improve efficiency and reduce commercial, industrial, logistics and administrative expenses.

The beef segment in Brazil and abroad, continued to suffer from the slow recovery of the herds, reducing the supply of cattle for slaughter and pushing up raw material costs. In addition, the exchange rate had a negative impact on exports in the year through September.

Given this scenario, in order to align production with variations in demand in the domestic and export markets, while pursuing maximum operating profitability, the Company implemented several operational adjustments, through which it reached a consolidated capacity utilization rate of 66%, versus 65% in 2010. At year-end, nine plants were temporarily closed, seven of which in Brazil, one in Argentina and one in Uruguay. Production was transferred to other industrial units, optimizing use of the industrial facilities in South America, diluting costs and improving performance.

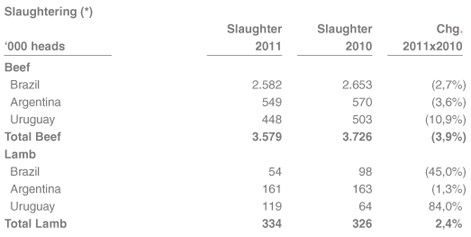

Marfrig slaughtered 2.6 million head of cattle in Brazil in 2011, 2.7% less than the previous year, while total slaughter volume in the country fell by 1.8%. The Company recorded a 12.0% share of total national slaughter volume, versus 12.1% in 2010 (considering only those cattle inspected by the Ministry of Agriculture, Livestock and Supply - MAPA).

In Argentina and Uruguay, slaughter volume fell 3.6% and 10.9%, respectively, due to market conditions in these countries and higher finished cattle prices.

(*) Total volume of beef production does not refer to slaughtered volume only. To optimize costs, the company may opt to purchase carcasses for deboning. Marfrig does not disclose purchased carcass volumes, since this is regarded as strategic information.

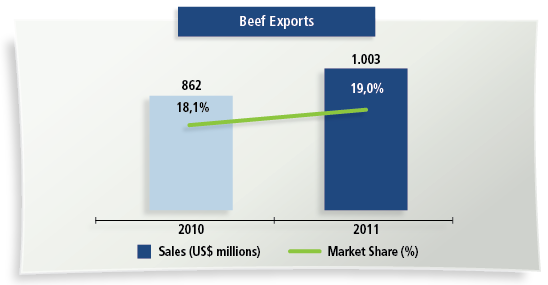

The average market share of beef exports (US$) was 19.0% in 2011, having peaked at 25.8% in April, versus 18.1% the year before. Due to heated demand in Brazil, part of scheduled export volume was rerouted to the domestic market in the third and fourth quarters.

Graph 12 - Marfrig’s share of Brazil’s total beef exports (Source: Secex).

Given the positive outlook for the cattle cycle in the coming years, as well as the buoyant domestic market and the gradual increase in exports due to improved exchange parity, the Company will continue with its strategy of expanding capacity utilization in Brazil. It will also be focusing on higher value-added products under the Bassi and Seara brands (such as the Seara Angus and Seara Cordeiro lines, developed and recognized for their exemplary tenderness, flavor and succulence), as well as the more profitable sales channels and markets.

Operations in Argentina faced a challenging scenario in 2011, with a more than 30% upturn in live cattle prices in local currency, according to ONCCA, price controls on fresh cuts in the domestic market, and restrictions on exports. However, Marfrig’s strategy of focusing on market niches and increasing production of processed items, in addition to the introduction of the Seara brand, offset these difficulties and enabled the Company to close the year with average capacity use of around 62.0%.

In 2012, with the shrinkage of operations in Argentina (due to the exchange of assets announced in December 2012), Marfrig will continue to route output to specific market niches and exports, while seeking synergies with the Group’s other operations and complementing its portfolio by launching Seara poultry, pork, prepared and processed products to meet increasing Argentinean demand for these items. In the export market, the Company will continue to concentrate on value-added prime cuts and attempt to use its entire Hilton quota (Marfrig has the highest Hilton quota in South America).

Marfrig is the largest privately-owned company in Uruguay and will continue to benefit from its leadership position and the country’s excellent animal-health conditions to boost exports. Currently, Uruguay is authorized to export beef to countries that restrict beef imports from Brazil and Argentina.

The gradual increase in finished cattle supply at the close of 2011 should continue in 2012, leading to healthier better prices and a gradual margin recovery. The Company’s intention in this segment is to:

• Increase plant utilization rate at the plants, thereby improving margins, even if this results in a certain reduction in production volume;

• Focus on products with more profitable brands and markets; and

• Focus on specialized channels, such as food service.

8. Investments

Most of the year’s programmed investments were disbursed in the first six months, mainly due to the projects begun in 2010. In 2012, investments in fixed assets should follow the downward trend observed in the second half 2011.

Below is a breakdown of the Marfrig Group’s investments in 2011.

9. Capital Structure, Liquidity and Ratings

Consolidated of Debt

The Company’s consolidated gross debt increased by R$ 2,034.3 million, while cash and cash equivalents fell by R$ 399.4 million, reflecting period investments of R$ 948.5 million, as well as investments in working capital to increase beef plant capacity utilization rates and boost sales at Seara.

The leverage ratio (net debt of R$ 7,785.1 million) stood at 4.39x. In terms of currency, 23.5% of the gross debt was denominated in Reais and 76.5% in other currencies, in line with revenue generated in currencies other than the Real in 2010, which came to 74.3% of the total.

At the close of 2011, 20.8% of the debt was short-term, versus 30.9% in 2010. In 2012, the Company will continue to manage its capital structure, with a focus on long-term operations. At year-end, cash and cash equivalents came to R$ 3,477.0 million, 10.3% down on the R$ 3,876.4 million recorded at the close of 2010, sufficient to cover 1.48x short-term debt of R$ 2,342.1 million (versus 1.4x last year).

Operations to finance the company’s investments in 2011 and adjust the debt profile included an R$ 600 million non-convertible debenture issue in March, maturing in 2013, 2014 and 2015, and a US$750 million senior notes issue maturing in 2018, with a coupon of 8.375%.

Global Risk Rating

In October 2011, the risk rating agencies Moody’s and Standard & Poor’s reaffirmed their respective ‘B1’ and ‘B+’ ratings, but revised their long-term outlook to negative in a year characterized by a challenging macroeconomic scenario, with high commodities prices and international demand impacted by the global economic crisis.

In December 2011, Fitch maintained its ‘B+’ rating, with a stable outlook, in both local and foreign currencies, thereby confirming confidence in Marfrig’s ability to capture synergies, reduce its working capital needs and optimize its capital structure.

10. Capital Markets

Capital Stock

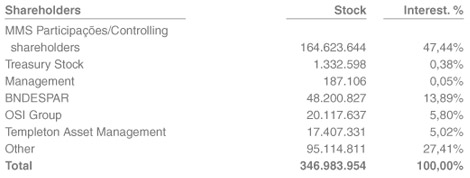

Marfrig’s subscribed and paid-in capital, comprising a single class of 346,983,954 common shares, totaled R$ 4,061.5 million on December 31, 2011.

Ownership Structure

In October 2011, the controlling shareholders of Marfrig Alimentos S.A., encouraged by confidence in the Company’s solid fundamentals and substantial potential value creation, began to acquire Marfrig shares through the BM&FBovespa, with a consequent increase in their stake.

The following table shows Marfrig’s ownership structure on December 31, 2011, considering shareholders owning more than 5% of the capital stock:

Consolidated position on December 31, 2011.

3rd Issue of Simple, Non-Convertible Debentures

On March 4, 2011, Marfrig Alimentos concluded the subscription and paying in of its 3rd Issue of Non-Convertible Debentures, which were the object of public distribution with restricted placement efforts. A total of 598,200 debentures were subscribed, with a nominal unit value of R$ 1,000.00.

With the intention of maintaining its debt profile, and given that more than two-thirds of its revenue is in foreign currencies, the Company opted to undertake a swap transaction whereby the First Series Debentures (remunerated at 127.60% of the DI interbank rate) and the Second Series Debentures (IPCA inflation index + 9.5% p.a.) would be pegged to the variation in the U.S. dollar exchange rate + fixed interest of 6.98% p.a.

Senior Notes Issuance

On May 9, 2011, Marfrig concluded a US$750 million, 7-year senior notes offering through its subsidiary Marfrig Holdings (Europe) B.V. The bonds, which mature on May 9, 2018, were issued with a coupon of 8.375% and assigned a foreign-currency risk rating of B1 by Moody’s and B+ by Standard & Poor’s and Fitch. The operation was guaranteed by Marfrig Alimentos S.A. and its subsidiaries Seara Alimentos S.A., Unifred - União Frederiquense Participações Ltda. and Marfrig Overseas Limited. The notes were acquired by an extensive range of prime investors in the United States (41%), Europe (39%), Asia (10%) and Latin America (10%).

Stock Performance in 2011

Marfrig’s shares are listed under the ticker MRFG3 in the BM&FBovespa’s Novo Mercado trading segment and are also included in the theoretical portfolios making up the following indexes:

• Ibovespa - Bovespa Index;

• IBrX - Brazil Index;

• IBrX-50 - Brazil Index 50;

• IGC - Special Corporate Governance Stock Index;

• ITAG - Special Tag Along Stock Index;

• INDX - Industrial Sector Index;

• SMLL - Small Cap Index;

• ICON - Consumption Index; and

• ICO2 - Carbon Efficient Index, created by the BM&FBOVESPA and the Brazilian Development Bank (BNDES) to promote the management of climate change by publicly-traded companies.

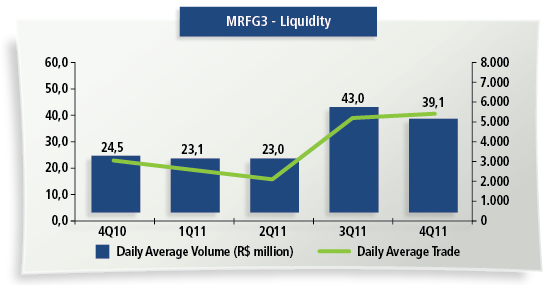

Daily traded volume averaged R$ 32.1 million in 2011, versus R$ 27.0 million in 2010, from an average of 3,641 daily trades, versus 2,584 the year before. Marfrig’s shares closed the year at R$ 8.54, 44.7% down on the end of 2010, mainly due to the withdrawal of the GWI Funds from our shareholder base, as explained below. In the same period, the Bovespa Index fell by 18.9%.

Graph 13 - Marfrig’s liquidity trends in 2010 and 2011, according to the BM&FBovespa.

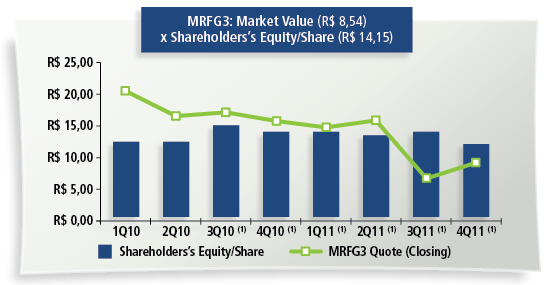

In August 2011, the Company announced a reduction in the relevant interest held by the funds managed by GWI Asset Management S.A., which, together with the uncertainties surrounding the global economic scenario, led to oscillations in the Company’s market share price, which averaged R$ 8.54 in 4Q11, versus its book value of R$ 14.01.

(1) Adjusted by the maximum number of shares corresponding to the convertible

debentures after the conversion (in 2015), totaling 449,024,770 shares.

Graph 14 - Comparative changes in the market value and book value of Marfrig’s shares since 2010.

11. Corporate Governance

Overview

Marfrig is committed to best corporate governance practices and adopts the highest standards of transparency in regard to all its stakeholders: shareholders, investors, clients, consumers, suppliers, employees and society as a whole. Since it is a publicly-traded company, it complies with the rules established by Brazil’s Securities and Exchange Commission (CVM) and Securities, Commodities and Futures Exchange (BM&FBovespa). It also follows the recommendations of the Brazilian Code of Best Corporate Governance Practices, as prepared by the Brazilian Corporate Governance Institute (IBGC), in the belief that continuous improvements in these practices increase the Company’s value and improve its performance. As recognition of its governance practices, in September 2011 Marfrig was one of the winners of the 2011 Transparency Trophy granted by Anefac, Fipecafi and Serasa Experian. This award also marked the first entry of a food company into the select group of 15 most transparent publicly-held companies.

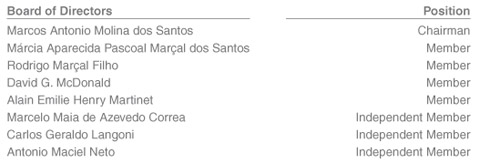

Board of Directors

Marfrig’s Board of Directors currently consists of eight members, three of whom are independent members. A detailed breakdown of the Board of Directors can be found in item 18.

Permanent Fiscal Council

The objective of the Fiscal Council is to oversee Management’s activities and give opinions on certain issues. The installation of Marfrig’s Fiscal Council was approved by the Annual Shareholders’ Meeting.

As announced in the Minutes of the Fiscal Council disclosed on December 21, 2011, Estefan George Haddad, a sitting Fiscal Council member elected on April 30, 2011, resigned from his position in favor of his alternate, Peter Vaz da Fonseca, thereby preventing any conflicts of interest, in order to take up an executive position with the auditing firm BDO RCS. As a result, on December 31, 2011, the Fiscal Council consisted of three members and two alternate members, one of whom appointed by minority shareholders holding more than 5% of the Company’s capital stock. A breakdown of Marfrig’s Fiscal Council is shown below.

Support Committees

The company currently has three committees to support the Board of Directors, who hold monthly meetings to implement initiatives aimed at ensuring the adoption of best corporate governance practices. The following independent Board of Directors’ members were appointed to coordinate the committees:

• Audit Board: Marcelo Maia de Azevedo Correa;

• Finance Committee: Carlos Geraldo Langoni; and

• Compensation, Governance and Human Resources Committee: Antonio Maciel Neto.

Code of Ethics

Marfrig’s Code of Ethics establishes the values, principles and attitudes to be adopted by its employees. Based on moral values that go beyond mere compliance with the law, the Code envisages the paths, attitudes and commitments that will ensure Marfrig’s reputation and integrity in the conduct of its business and processes throughout the entire chain, from relations with suppliers and the acquisition of production raw materials, through relations with the environment and its surrounding communities, to commercial and institutional relations with clients, consumers and shareholders. Employees, suppliers, clients and other stakeholders can consult the Code on the Company’s website (www.marfrig.com.br/ri), as well as make suggestions or denounce breaches.

Stock Option Plan

The Company also maintains a Stock Option Plan, which aims to allow directors, executive officers, employees and service providers of the Company or its subsidiaries to acquire Marfrig stock, subject to certain conditions, in order to: (a) promote the expansion, success and execution of the Company’s objectives; (b) align the interests of the Company’s shareholders with those of its directors, executive officers, employees and service providers or those of its subsidiaries; and (c) enable the Company or its subsidiaries to contract and retain directors, executive officers, employees and service providers.

In December 2011, 147 employees were included in the Stock Option Plan, which is available on the Company’s website (www.marfrig.com.br/ri) and the website of the Securities and Exchange Commission of Brazil (www.cvm.gov.br).

Trading Policy

The Marfrig Alimentos S.A. Securities Trading Policy establishes the rules and procedures to be adopted by the Company and its related persons in regard to trading in securities issued by Marfrig, assuring all stakeholders of ethical conduct by those with access to material information. The Policy also seeks to prevent and punish the improper use of privileged information by those with access to it. The Securities Trading Policy is available on the Company’s website (www.marfrig.com.br/ri) and on the website of the CVM (www.cvm.gov.br).

Risk Management

The Company is subject to market risks in its activities related to fluctuations in exchange rates, interest rates and commodity prices. In order to mitigate these risks, the Company establishes policies and procedures to manage such exposures, and can use hedge instruments, as long as these have been previously approved by the Finance Committee. In addition, the Group’s geographic, portfolio and market diversification strategies are closely aligned with its risk management policy. Geographic and portfolio diversification allow the Company to proceed with its operations without being unduly affected by sanitary or economic barriers, or major oscillations in product and raw material prices or costs.

12. Social and Environmental Responsibility

The Marfrig Group strives to become a benchmark for sustainability in its market segment. In order to do so, it adopts a policy of continuous improvement and technological innovation, underpinned by the transparency of its activities and corporate governance practices.

The pursuit of business sustainability is one of the pillars of the Marfrig Group’s strategy, and is reflected in the expansion of its activities, always based on the triple bottom line concept, i.e. social, environmental and economic aspects (or, more commonly, people, the planet and results). Marfrig is committed to maintaining this balance, respecting the cultural aspects, business practices and local characteristics of each unit.

In this context, in 2011 Marfrig undertook the first global mapping of its GHG emissions throughout the entire production chain. This resulted in the first global emissions report, which will serve as a platform for the implementation of a series of environmental programs designed to lead us towards a low-carbon economy. We also prepared our first Annual Sustainability Report based on Global Reporting Initiative (GRI) guidelines.

The Marfrig Group regards sustainable development as an ethical means of conducting its businesses and creating long-term value, involving all its stakeholders, including clients, consumers, suppliers, partners, employees, shareholders, investors, financial institutions, society and the government.

By adhering to the main public commitments related to corporate sustainability in the sector, the Group is demonstrating its proactive approach to anticipating solutions rather than merely reacting to legal requirements.

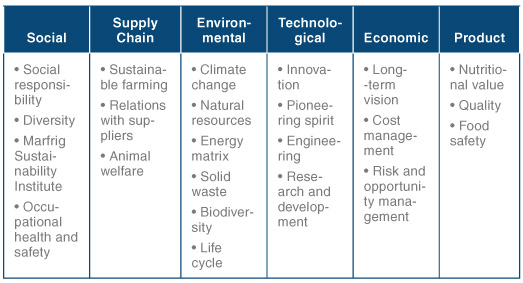

The Corporate Sustainability Strategy, which permeates all the group’s divisions, comprises six fronts supported by 23 pillars, as presented below.

The Group’s main sustainability initiatives are available on the company’s Sustainability website www.marfrig.com.br/sustentabilidade.

13. People Management

In 2012, Marfrig announced a new, streamlined corporate structure developed jointly with Bain & Company, in order to ensure a better focus and strategic support for the management of its businesses, as well as the proper appreciation of its human capital.

In 2011, the Group unified its HR practices and policies with the aim of consolidating its segments, investing in professional training and development, encouraging participatory management and promoting the formation of leaders across all the divisions.

The occupational health and safety guidelines were enhanced in order to reduce employees’ exposure to the risk of occupational accidents and illnesses. In Brazil, internal campaigns were launched to combat dengue fever, breast cancer and osteoporosis, in addition to campaigns to collect winter clothing, school supplies and donations for victims of environmental disasters.

The Marfrig Group’s Code of Ethics is followed by all industrial, commercial and administrative units in all the countries where the Company operates, enabling the formation of a unique and global culture, guided by the same social and environmental values.

The Group’s management practices as applied to its employees and external stakeholders, put it in the forefront in regard to the handling of its myriad national and international relationships. The company complies with all the requirements of the World Labor Organization (WLO), as well as the legislation of the countries where it operates, develops safety awareness campaigns and training courses on the correct use of personal protection equipment and registers all occupational accidents and illnesses.

Employees

The Marfrig Group ended 2011 with 84,535 employees worldwide, 6.7% less than in 2010, mainly due to the adjustments in Brazil, in turn caused by the temporary closure of certain plants and the reduction in working shifts in order to optimize capacity use and margins. The table below shows the number of employees by division:

(1) Includes employees of Marfood (USA) and Chile.

(2) Includes employees of MoyPark and Keystone.

Of this total, 59% are male and 41% female, identical to the 2010 ratio. Since Marfrig is relatively young, 66% of its employees have been with the Company for up to five years, 19% for between five and ten years, and 15% for more than ten years.

In terms of age, 57% are 35 years old or younger, 36% are aged between 25 and 35, and 43% are older than 35.

The Company’s average monthly turnover is 3.64%, 15 bps/month less than in 2010.

Net revenue per employee grew by 21.4% over 2010.

(*) On December 31, 2011.

14. Guidance

Given the unstable macroeconomic conditions, as well as FX and raw material price volatility (cattle and grains), Marfrig opted not to disclose its guidance for 2011 and 2012.

15. Commitment to Arbitration

The company, its officers and members of the board of directors are committed to resolving through arbitration any dispute or controversy arising between them relating to or originating from, in particular, the application, validity, effectiveness, interpretation, breach and their effects of the provisions contained in the Novo Mercado Listing Agreement, the Novo Mercado Listing Regulations, the Bylaws, Brazilian Corporation Law, the regulations issued by the National Monetary Council, the Central Bank of Brazil or the Securities and Exchange Commission of Brazil (CVM), the regulations of the São Paulo Stock Exchange (BM&FBOVESPA), other rules applicable to the functioning of the capital markets in general, the Arbitration Commitment and the Arbitration Regulations of the Market Arbitration Chamber, with said arbitration conducted in compliance with these latter Regulations.

16. Relations with the Auditors

Pursuant to CVM Instruction 381/2003, which refers to relations with our independent auditors - KPMG AUDITORES INDEPENDENTES and BDO abroad Brazil - we hereby declare that fees related to services other than those associated with the independent audit accounted for less than 35% of the total fees paid by Marfrig Alimentos S.A. and its subsidiaries to the auditors.

17. Subsequent Events

• On January 30, 2012, Marfrig announced the new CEO of Seara Alimentos, David Alan Palfenier. Mr. Palfenier is 55 years old and holds a degree in Business Administration, with a major in Marketing, from Eastern Washington University. Previously, he was CEO of ConAgra Foods, Consumer Foods International, and replaced Mayr Bonassi as CEO of Seara as of February 2012. Mr. Bonasssi, who headed the Marfrig Group’s Poultry, Pork, Prepared and Processed Product operations in Brazil for five years, announced his retirement at the end of 2012. Until then, he will ensure a smooth hand-over of the reins to his successor and serve as a member of the company’s Advisory Council.

• On January 31, 2012, Marfrig announced an accident at its tannery in Bataguassu (MS), which was isolated for forensic examination. Preliminary information indicates that there was a chemical reaction during the unloading of inputs by an outsourced company. The Bataguassu unit’s meatpacking and beef processing unit, which is located near the tannery, was not affected by the accident.

• On February 13, 2012, the company announced the conclusion of the due diligence process and the execution of a final and irrevocable agreement for the sale of its specialized fast-food logistics service businesses in the USA, Europe, the Middle East, Asia and Oceania of its subsidiary Keystone Foods, LLC to The Martin-Brower Company, L.L.C. The total price of the assets and businesses was confirmed USD400 million.

• On February 27, 2012, the Company announced its new organizational structure, approved by the Board of Directors in a meeting held on the same date, through the constitution of a new business unit, Seara Foods, whose objective is to guarantee greater integration and generate more synergies in the Group’s poultry, pork, prepared and processed product segment, comprising Seara, Moy Park and Keystone Foods. Despite the integration, the three units will continue operating with their own identities, and the alterations in the division and in the holding company will not change the financial information disclosure format currently adopted by Marfrig Alimentos S.A.

• On March 20, 2012, the Company announced together with BRF - Brasil Foods S.A., in addition to the Notice of Material Fact released in December 08, 2011, the signature of a Asset Exchange Contract and Other Covenants, establishing the terms and conditions for the transaction of the assets arising from the Performance Commitment Agreement (Termo de Compromisso de Desempenho - TCD).

The transaction aims to strengthen the Seara brand in Brazil’s domestic market, which include doubling our production capacity of elaborated and processed products, increasing our market share and allowing these products to reach a higher number of consumers while ensuring high levels of quality, safety and agility.

The transaction implementation is subject to the approval of the Administrative Council for Economic Defense (“CADE”).

18. Board of Directors

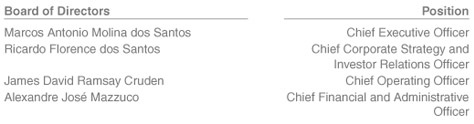

19. Board of Executive Officers

20. Declaration of the

Ceo

I, Marcos Antonio Molina dos Santos, hereby declare that: 1 - Based on my knowledge, the planning presented by the auditors and the subsequent discussions of the auditing results, I have reviewed and fully agree with the opinions expressed in the report prepared by KPMG Auditores Independentes. 2 - I have reviewed this report of the Financial Statements of MARFRIG ALIMENTOS S.A. for the fiscal year ended December 31, 2011, and based on the subsequent discussions, I agree that said Statements accurately reflect all material aspects and the financial positions for the periods presented.

São Paulo, March 23, 2012

Marcos Antonio Molina dos Santos

21. Declaration of the Investor Relations Officer

I, Ricardo Florence dos Santos, hereby declare that: 1 - Based on my knowledge, the planning presented by the auditors and the subsequent discussions of the auditing results, I have reviewed and fully agree with the opinions expressed in the report prepared by KPMG Auditores Independentes. 2 - I have reviewed this report of the Financial Statements of MARFRIG ALIMENTOS S.A. related to fiscal year ended December 31, 2011, and based on the subsequent discussions, I agree that said Statements accurately reflect all material aspects and the financial positions for the periods presented.

São Paulo, March 23, 2012

Ricardo Florence dos Santos

22. Declaration of the Chief Operating Officer

I, James David Ramsay Cruden, hereby declare that: 1 - Based on my knowledge, the planning presented by the auditors and the subsequent discussions of the auditing results, I have reviewed and fully agree with the opinions expressed in the report prepared by KPMG Auditores Independentes. 2 - I have reviewed this report of the Financial Statements of MARFRIG ALIMENTOS S.A. related to fiscal year ended December 31, 2011, and based on the subsequent discussions, I agree that said Statements accurately reflect all material aspects and the financial positions for the periods presented.

São Paulo, March 23, 2012

James David Ramsay Cruden

23. Declaration of the Chief Financial and Administrative Officer

I, Alexandre José Mazzuco, hereby declare that: 1 - Based on my knowledge, the planning presented by the auditors and the subsequent discussions on the auditing results, I have reviewed and fully agree with the opinions expressed in the report prepared by KPMG Auditores Independentes. 2 - I have reviewed this report of the Financial Statements of MARFRIG ALIMENTOS S.A. related to fiscal year ended December 31, 2011, and based on the subsequent discussions, I agree that said Statements accurately reflect all material aspects and the financial positions for the periods presented.

São Paulo, March 23, 2012

Alexandre José Mazzuco

|